Investment Management

Smart Investing. Personalized To You.

Featured In

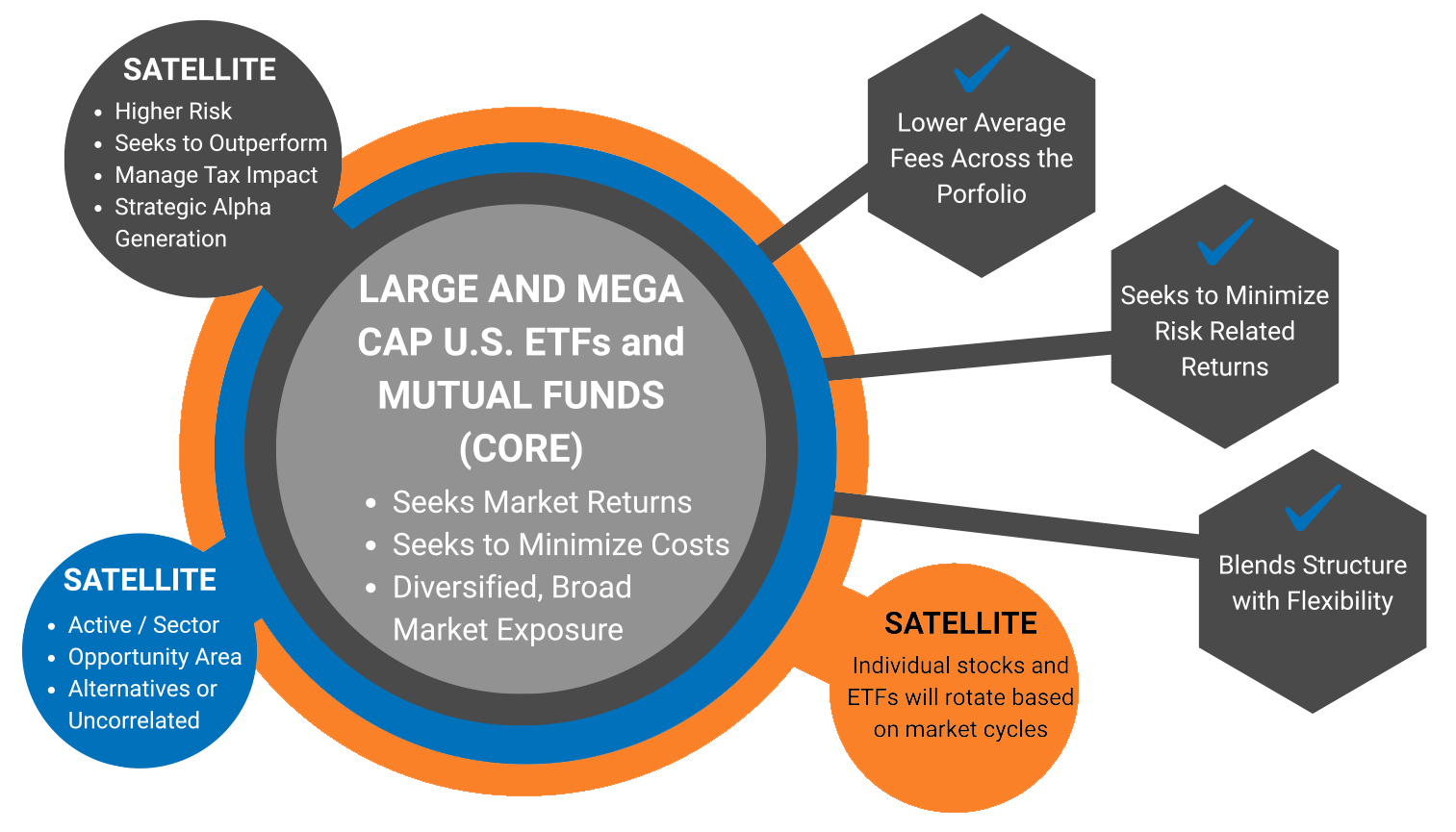

You’ve built something meaningful and managing it wisely matters more than ever. At Chesapeake, we use a Core & Satellite investment philosophy designed to keep you grounded and growing, even as markets shift.

Your “core” investments are built for long-term strength and stability, efficient, evidence-based, and tailored to your goals. Around that, we position “satellites” to adapt to opportunities, manage tax impact, and respond to what life or the market throws your way.

It’s a strategy that blends structure with flexibility, so you’re never stuck chasing headlines or making guesses in a vacuum. You stay in control, supported by a fiduciary team that explains the why, not just the what, behind every move.

Core Satellite Philosophy

Who Holds Your Assets Matters

When you're trusting someone with your wealth, it's not just about who manages your investments but who safeguards them.

At Chesapeake, we’ve chosen to partner with LPL Financial as our custodian, because your financial security deserves strength, scale, and transparency. LPL is not a bank, product manufacturer, or insurance company and that matters. We remain independent fiduciaries, free to focus solely on what’s best for you, not on selling proprietary products or meeting quotas.

Our role is to help you navigate financial complexity with clarity. LPL's role is to provide a secure foundation behind the scenes, so you can move forward with confidence.

You stay in control. We stay accountable. Together, we use LPL’s robust platform to help you build a portfolio that serves your goals, not someone else’s.

Why LPL?

💼 Over $1.9 trillion in brokerage and advisory assets serviced or custodied

🔒 Cyber Fraud Guarantee: 100% reimbursement for losses due to unauthorized access

🏦 SIPC + FDIC Protection: Account coverage up to $500K (SIPC), with additional FDIC insurance through multi-bank

👥 29,000+ independent advisors use LPL’s platform to serve clients with integrity

🧭 Zero proprietary product push—your advisor recommends what’s right for you

💪 Fortune 500 company (#340 in 2025), with the scale to protect and support your investments

Our role is to help you navigate financial complexity with clarity. LPL's role is to provide a secure foundation behind the scenes, so you can move forward with confidence.